If one wants to be rich, one should learn how to invest on your own…right ? that way you can compound your capital and retire rich ! Isnt that obvious ?

If I am asking this question, you can guess I don’t believe it to be the case.

I get asked this question in different shapes and forms and a typical email goes like this

Rohit – I am currently X years old and want to become financially independent in the next 10 years so that I can purse XYZ (insert a dream here). Can you suggest how to become a better investor so that I can have enough money in a decade to pursue my dream ?

What does it take to be an active investor ?

It takes a few hours a week for a year or so to become financially literate, which involves having a reasonable understanding of various investment options such as fixed deposits, mutual funds, stocks, and insurance etc. Once you reach this level of understanding, you can with a moderate amount of effort, identify a mix of assets which will help you earn around 12-14% return per annum (depending on the mix of debt and equity)

In effect, you can spend a few hours a month and earn 12-14% on your assets over the long term. We can call this a baseline level of effort.

Now lets assume that you are not satisfied with the above returns and would not settle for anything less than 20%+ levels (around 10 times in the 10 years). If you wish to achieve these level of returns, then you need to invest atleast 15+ hours a week on learning various aspects of investing and in finding new opportunities on a regular basis.

What is the return on time in case of active investing?

So what do I mean by the term – Return on time ? Let me illustrate with an example.

Let’s look at a typical case of a young professional who has a full time job. Let’s assume the following

Annual salary in year 1 = 10 lacs

Annual savings in year 1 = 5 lacs (I know this is too high, but we are considering an optimistic scenario)

Salary increases each year by 10% and so does the savings. This individual has two options for his/ her savings. They can be financially literate and spend minimal time (a few hours a month) and earn around 12-14% per annum or spend 15 hrs or more on investing and earn a much higher return.

Lets also assume the individual works around 40 hrs each week in his / her job (would be higher in reality)

So whats does the return on time (money earned per hour spent) look like for the person in terms of active investing ?

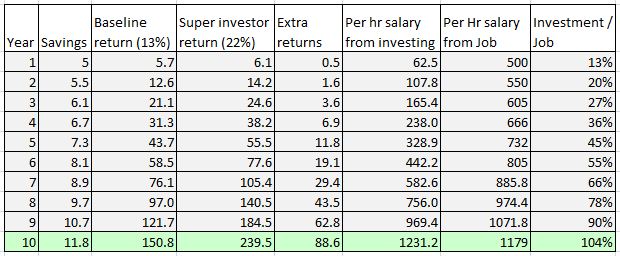

Lets look at the table below

I have plotted the savings, the extra returns earned by putting in extra hours each week (15 hrs per week) and the per hour return

A few things standout,

In the initial years when one has a small level of savings and is just starting out, the per hour ‘salary’ from investing is way below the per hour salary from a job. The higher your education or skill, the larger the gap.

This is the best case scenario. The above picture worsens if one gets hit by a bear (a certainity in a 10 year period). The last column shows that this ratio becomes favorable only after 8-9 years

Implications of the analysis

The above analysis though silly, lead us to a fairly important conclusion. If the only reason you want to become an active investor is to make more money, then it is not a very smart way to do it.

For starters, all the time spent in the initial years will appear to be a complete waste of time. Most of the people soon realize that the extra returns are really not worth the time.

In addition, if you start late in a bull cycle (as most individuals do), the quick and easy returns are soon lost in the subsequent bear market. In most cases, such individuals throw in the towel and move on to other pursuits in life.

Finally, the additional hours spent on investing means that one does not have time for any other pursuits like having girlfriends or other hobbies at the prime time of their life (early to late 20s).

My personal story

The above table and discussion is not theoretical. I have personally lived it for the last 15 years. I started investing in the late 90s (around 1997). I think I was financially literate by around 1998 and around that time came across the book – The warren buffett way. I read about this person who had become the second richest person by investing in stocks and was completely mesmerized by it.

I read the biography of warren buffett (Making of an American capitalist) and his letter to sharehlolders and anything else I could find about him. It was in late 1999 , early 2000 that I finally turned to active investing.

As you can see, my timing was perfect. I made some money for around 3-4 months of 2000 and then lost all the gains by the end of year – some on paper and some of it was a permanent loss as I had put money in IT/ Internet oriented mutual funds (don’t ask what I was thinking).

The years from 2000-2003 was one long bear market, where the market slowly went down from 4000 levels to around 3000 in a period of three years. If I put the numbers in the earlier table, my ‘salary’ from investing was negative, whereas I was making a good income from my full time job.

Any rational person after three year of losing money, would have given up investing and move onto something else in life. I did not even think of it as I was extremely passionate about it and inspite of mediocre absolute returns, I was still beating the market by a large margin.

The market turned in mid 2003 and as it took off for the next 5 years, so did my portfolio.

Better way to well

As you can see from my personal experience and from the analysis, that investing is definitely not a quick or easy way to becoming rich.

Let me suggest an alternative – If you are really passionate about something or good at your full time job, focus on it and get better at it. You will have fun doing it and over a decade you will make a decent amount of money out of it. Invest the money saved, sensibly by becoming financially literate and you will realize that not only is your life more pleasant , but that you also have enough tucked away for a rainy day.

I know this is not the conventional wisdom and we have a cottage industry of people encouraging others to invest on their own. I would rather follow my interest/ passions and become good at it (the money usually follows then), than do something just for the sake of a little extra money.

In case you wondering about the life I had outside work and investing early on …I am not going to disclose than on my blog and get in trouble with my wife J