Now, before I start crowing, let me come clean on a few points. The Kesar enterprise arbitrage idea was brought to me by ninad (see his blog here). I was smart enough to get on the ride.

This deal was announced in March and it took around 9 months for the deal to complete. I have also listed some thoughts and analysis (which include substantial inputs from ninad) over the course of the deal at various points of time

Basic idea

Kesar enterprise is a sugar company with a division which was expanding into the warehousing and other port related infrastructure such as storage. The company announced in Dec 2009 that they would be demerging the infrastructure business. You can find the announcement here.

I am posting my personal notes on the deal below

De-merger evaluation – March 19th

Kesar enterprises has announced the de-merger of its Sugar biz from the Infrastructure warehousing biz.

The numbers for each biz is as follows (in crs)

Warehouse/ transport divison

Revenue: 16 Crs (2010 expected)

PAT: 7-8 crs

Return on assets – 30%+

Valuation – around 60-70 crs minimum

Sugar divison

Revenue – 285 crs gross including excise

PAT – 2-3 crs.

Over 10 years the company has made very small profits. So difficult to value based on profits.

Inverting the problem – Mcap of the company is 82 crs. So is the sugar biz atleast 20-30 crs?

Alternative valuations

Book value – 40-50 crs (after all debt). So liquidation value is higher

Comparative valuation – based on price / sales, most of companies in this sector are priced around 1-2 times. Due to poor profitability, we can price this company at 50% of sales – 100 crs?

On capacity basis, a comparable company like dhampur sugar (UP based company), sells for 0.011 Crs/ TCD. Kesar enterprise sugar business can then be valued at 80 crs.

So total conservative value is around 140-200 crs.

Action plan – create initial position at 120 levels

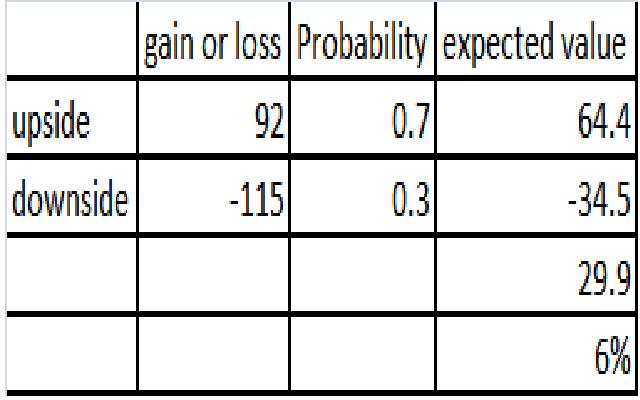

Negative case – March 30th

Sugar prices tumbling and market has caused the stock prices to drop by 30% in feb and march. Kesar has seen stock price drop by 10-15%.

2011 will see surplus sugar and hence the futures have started going down. Stock prices could drop

further – if that is the case, delay increasing the position, close to the ex-date as possible

Debt getting split – more to infra company: need to track this

Midcap discount – look at midcap futures to hedge?

How to hedge against drop in sugar industry – can use puts on Balrampur chini and Bajaj Hindustan

Stock goes ex-date – May 19th

The ex-date was 14-May. The sugar business has dropped to around 50 rs which gives a mcap of 30 crs. The sugar biz is in down cycle and hence the prices for all companies have crashed

Key mistake and learning – did not hedge on the down turn in sugar as I was thinking on 30-march.

Action plan – wait for upturn in sugar to exit the sugar biz. A sale at 60 and higher should work out in the deal. May have to sustain further drops before recovery.

Kesar enterprise stock recovers – Sept first week

Price now at 70 levels. Sell the stock!!

Kesar infrastructure yet to be listed – Dec first week

Was able to sell the sugar piece @65-70 prices. Deal which was expected to take 4-5 months at max has taken twice that amount – around 9 months already. No updates yet.

Stock finally listed – Dec 22nd

Kesar infrastructure finally listed at 99. A gain of 30% in nine months. May hold on to the stock

Key learnings

· Such arbitrage deals take longer than expected. Patience is the key here

· One cannot ignore short term implications on the stock price and treat it as a long term idea. If possible, options can be used to hedge the position only if the timelines are certain

· Build the arbitrage position over a period of time and not immediately after the announcement as the price drifts downwards once the buying/ selling pressure subsides