I had done a quick valuation exercise of MRO-TEK earlier (see here). I used a certain PE ratio in the post and said that I would explain my approach later. So here it goes …

I had done a quick valuation exercise of MRO-TEK earlier (see here). I used a certain PE ratio in the post and said that I would explain my approach later. So here it goes …

To understand my approach, you have to look at the file Quantitative calculation and worksheets – cap analysis and ROC and PE. You download this file from the google groups

The worksheet ‘ROC and PE’ has DCF (discounted cash flow model) scenarios for various businesses such as Low growth, high ROC (return on capital ). For ex: Like Merck or high growth and high ROC like infosys etc.

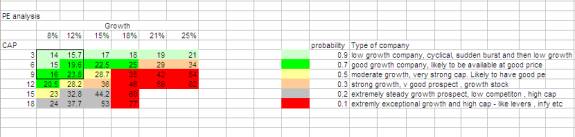

Now I have used various assumptions of growth, ROC etc and created the matrix below (CAP analysis worksheet in the same file)

{kind=link}

As you would expect, if growth increases, so does the intrinsic value and the PE. If the ROC increases the same happens. This is however ignored by most analysts and sometimes the market too. This is where opportunity lies sometimes. The third variable – CAP also behaves the same. Higher the period for which the company can maintain the CAP, higher the intrinsic value and higher the PE. CAP or competitive advantage period is not available from any annual report or data. It is the period for which the company can maintain an ROC above the cost of capital. For a better understanding of CAP, read this article – measuringthemoat from

google groups. It’s a great article and a must read if you want to deepen your understanding of CAP and DCF based valuation approach.As I was saying, CAP is diffcult to estimate as it depends on various factors such as the nature of industry, competitive threats etc. I usually assume a CAP of 5-8 years in my valuations. If it turns out to be more than that, then it serves as a margin of safety.

Now when I look at the company, I use the worksheet ‘ROC and PE’ and my thought process (simplified) is as follows

1. Look at ROC – does the company have an ROE or ROC of greater than 13-14% ? If yes, is it sustainable (this is subjective).

2. Use the above worksheet to select a specific ROC sceanrio.

3. What has been the growth for the company in the last 8-10 years. What is the likely growth (again subjective estimates).

4. What is the likely CAP? This is a very subjective exercise and requires studying the company and industry in detail. If the company checks out, I usually take a CAP of 5-6 years.

5. Plug the ROC, growth, CAP and current EPS numbers in the appropriate sceanrio and check the PE. That is the rough PE for the instrinsic estimate.

6. Check if the current price is 50% of the instrinsic value

7. Cross check valuation via comparitive valuations and other approaches.

If all the above checkout, it is time to pull the trigger.

In case the above has not bored you to tears, 🙂

Hi Rohit,I found your blog through Google Reader. It is very good. Although, I dint understand much of your financial calculations, I will start to follow your blog posts religiously.Nice blog entries.Thanks,Nithin.

thanks nithin..and feel free to ask any questions you have regardsrohit

Rohit,I recently completed the Dhandho Investor by Mohnish Pabrai and The little book that beats the market by Joel Greenblatt. I find it very amazing that they have reduced value investing to such a nutshell the it it too mechanical and too good to be true. That has forced me to rethink on my future investment strategies? Can you offer any comments abot their suggestion about the magic formula?

Hi kotyboth are very good books. both the authors have boiled down to the essence of valueinvesting in both the books.i use the magic formulae as a first stage filter to select investment ideas. however i am not comfortable investing entirely based on the magic formulae or any other purely mechanical approach.pabrai’s investment approach and philosophy has made me move more towards deep value ideas. also i prefer to follow his portfolio sizing approach too

I too agree with you on this. By the way, which site do you use to filter the stocks? ICICIDirect offers only some of the filters like P/E,ROCE, RONW etc. Also is the ROCE of ICICI same as the one spoken by Greenblatt? The one at Equitymaster does not include all the stocks.

i use icici direct for initial filtering only. however icicidirect data is not always correct. they do not adjust for splits and bonuses quickly in their database.regardsrohit

Hello rohit, Thanks for the blog on PE Ratio . How do we evaluate PE ratio of companies whose business is to invest in other companies stocks .They do not earn money directly , they do most sell/buy shares and other from dividends of other companies.their only value unlock comes from seeling investments . It also varies from time to time due to book value of investments is tabulated based on the market capitalisation. How we calculate the original value(using DCF) fro these companies . for e.g Vardhman Holdings , McHoldings, HB Portfolio, tata inv .is it the same methodolgy as u mentioned in ur blog fro PE ratio?

Hi sujtihi would not value these companies based on DCF. Such holding companies will have to be based on the value of their holdings. The key issues in that is- is the market value of the holdings inflated or not ?- what discount should you consider for arriving at the final value of the holding company.unfortunately there are no fixed answers for that.i will try to answer your question in more detail in another postregardsrohit

Dear Rohit,On going through your Quant sheet, I see that you have taken FCF as the diff between earnings and change in BV over the preceeding year. But as you will agree, change in BV signifies retaind earnings and therefore what you call FCF is actually dividend as per your formula

Hi cigarthat was a good observation on your part. my response is yes and no to your point.the worksheet has a lot of assumptions and some oversimplifications too. for ex: i have not considered deprciation in the calculations, asset turns etc.what you mention is true in usual circumstances. what is not invested will given out as dividend. In the case i have put, i am assuming that the company is holding back only what is required for maintenance capex. so the ROC remains the same. however this also is true only if the growth is assumed at 7-8%. above that it becomes incorrect.basically my calculations are a bit too conservative. another way would be to assume earnings=FCF and do the same exercise. the two numbers we get for the PE can be used as the lower and upper boundfinally the worksheet i have built is a very quick and dirty approach. i dont use it to arrive at the final values. I use the valuationtemplates to do a proper DCF and arrive at the valueregardsrohit

Rohit,I would agree to what you say if the earnings growth assumed was conservative (7-8%) range. But you sheet assumes 10% earnings growth and even 15% in some instances. Therefore it would be wrong to assume that the retained earnings are only for maintenence capex and dont fund any growth. In my opinion it would be good and conservative to average out earnings over the last 3-5 yrs to get rid of the depreciation problem (lumpy FA investment may average out) and assume a low growth rate. Your Opinions!I want to mail you something of your interest. Any mail id I can send to?

hi cigaryou have rightly pointed out the flaw in the model. to certain extent the error is mitigated by considering the terminal value. as i said, i use this model only for a very rough indicator. i follow a detailed DCF analysis to avoid such assumptionsyou can email me on rohitc99@indiatimes.com

I found your blog searching on Google. You are doing great job explaining fundamental analysis. I was always keen on how to do DCF and other stuff though i am learner. I email ID is dharmeshbangali@yahoo.com and my cell number is 9820564340. I would like to understand your analysis in detail. Can you please mail me your email ID? Cheers and god bless you. Dharmesh Bangali

Hi dharmeshmy email id is rohitc99@indiatimes.comregardsrohit

Hi Rohit,I am new to your blog and have not been able to find the files mentioned in your post in googlegroups. Will it be possible for you to email the same to me at catrupti2008@gmail.com, pl?Thank you.Regards,Trupti

Dear Rohit

I am looking at your blog in 2019- seems lost many years of value investing. I am unable to get your DCF sheet (not in the google group) mentioned in this post. Possible you can send me an email please

iitkgp.vg.rohit@gmail.com

Thanks- looking forward.

Regards

rohit