I have often written about experiments and failures in the past (see here, hereand here). These posts have usually involved a failed experiment or idea and my conclusions or learnings from it. It has been a case of inductive reasoning (going from the specific case to general principles).

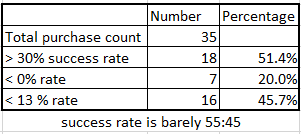

I recently initiated an exercise where I collated all the investments I have made since 2010/11 and analyzed the success rate of my picks. I have defined failure as a stock position which delivered less than 13% CAGR over the last 5-6 years.

Why 13% and not an actual loss? There are a few reasons behind it

– 13% is roughly the level of returns one can expect from an index and hence I have set that as the threshold

– It allows me to capture value traps as failures. These are stocks where the stock price has stagnated or trailed the index as I waited for valuations to revert to the long term averages.

The analysis was quite eye opening and although I had some vague idea of what to expect, the actual results were still surprising.

Surprisingly low hit rate

I have bought/ sold or held around 35 position in the last 6 years. Of these, I have lost money in 7 and consider 16 (or 45%) as failures (<13% category also includes the < 0% cases)

If you look at the above result, the conclusion could be that the overall portfolio has performed horribly. I am not going to share the actual results as that is not the purpose of the post and anyway I can claim anything in absence of independent verification. Let me just share that the portfolio has done substantially better than the common indices (substantial being 10% above the NSE 50 returns)

A common myth is that high returns need a 90%+ success rate (if not 100%).

The reason behind the myth

So why does almost everyone believe that one needs a perfect hit rate to achieve good returns? This myth is quite common as one can see from comments in the media, where people are surprised when some well-known investor has a losing position.

I think it speaks to the ignorance of the following points

– A losing position has a downside of 100% at the most, but a winning position can go up much more than that and cover for several such losses. Let’s say you have a portfolio of three stocks and two go to 0, but the third stock is a 5 bagger. Even in such an extreme example, the investor has increased his portfolio by 50% with equal weightage in all the three positions.

– Let’s take the previous example again and instead of equal weightage, let’s say the two failed position were only 10% of the portfolio, whereas the winning position was 90%. In such a happy scenario, the overall portfolio is up 4.5X.

In effect investors under-estimate the impact of upside from a winning position and the relative weightage of these winners. A portfolio is not like a true or false exam where every question gets the same marks. If you get something right, the weightage and extent of gain on that position matters a lot

So the next time, you read an article where some famous investor lost money on a position and chalk it to them being over-rated, keep in mind that the losing position could be a tiny starter position. A lot of investors sometimes start with a small position and then build it as their conviction grows.

The learnings

The main reason for this exercise was not to generate some statistics and leave it at that. I wanted to dig further and find some common patterns of failure. This is what I found

Blind extrapolation

The number no.1 failure for me has been when I assumed that the past performance of a company or sector would continue and hence the recent slowdown or poor performance is just a blip.

For example, I invested in a few capital good companies in 2010/11, assuming that the recent slowdown was just a blip. These companies appeared very cheap from historical standards and that motivated me to invest in some of them. I did not realize at the time, that the country was coming off a major capex boom and it usually takes 5+ years for the cycle to turn.

I have since then tried to dig deeper into industry dynamics and understand the duration of the business cycle of a company in more depth.

The forever cheap or value traps

These positions are a legacy of my graham style investing. These companies appeared very cheap by all quantitative measures. I would attribute the failure of these positions to the following reasons

–These companies were earning low returns on capital as the management had very poor capital allocation skills. To add insult to the injury, some of these companies refused to increase the dividend payout and just kept piling cash on the balance sheet. In all such cases, the market took a very dim view of the future of the company. Unlike the developed markets, India does not have an activist investor base and hence these companies end up going nowhere.

– I forgot to ask a very basic question: Why will the market re-value this company? What needs to change to cause this revaluation? In most of these cases, the company performance was not going to change substantially for a variety of reasons, and hence there was no reason for the market to change its opinion.

The turn which never happened

There have been a few positions where my expectation was the company will start growing again or will improve its return on invested capital (or both). In all such cases, the expected turn never happened and the company just kept plodding along with me incurring an opportunity loss during this time.

The problem with these kind of situations is that you don’t lose money due to which one is lulled into complacency. One fine day, after having waited for a few years, I realized belatedly that I was waiting for something which was unlikely to ever happen.

I have now changed my process to identify the key lead indicators for a company which need to change to confirm that the management is moving in the right direction. For example, is the management introducing new products, expanding distribution or trying something else to revive the topline? If the annual report and other communication continues to be vague on these points, it is best to exit and move on

Doing too much

There is another pattern I have noticed which is not obvious from the table. I have had a higher number of failures after a successful phase. I think this is most likely due to over confidence on my part which led to a higher number of new ideas in the portfolio with much lesser due diligence on each of them. The end result of this sloppy work was a much higher failure rate.

The changes

It is not sufficient to just analyze failure. One need to make changes to the process in order to prevent the same error from occurring again

Some changes in my process/ thinking has been

– It is difficult to invest in commodity/ cyclical stocks (atleast for me). I should tread cautiously and have a very strong reasoning behind such an investment (being cheap is not enough).

– Identify the reasons on why a company will be re-valued by the market. Also have a time frame attached to it (endless hope is not a strategy)

– Be your own critic. Confirm if the original thesis holds true? If not, exit. It is better to be proven wrong as quickly as possible.

– Growth is not all important, but absence of it can lead to a value trap.

– The most dangerous phase is right after a successful stretch. Resist the urge to extend your lucky streak by making investments into half-baked ideas. Take a break or vacation!

If there is one lesson from the above analysis you should take, it is that one does not need to have a very high hit rate to get decent returns. As long as one holds on to companies which are doing well and culls the poor performers rationally, the overall results will be quite good.

—————-

Stocks discussed in this post are for educational purpose only and not recommendations to buy or sell. Please contact a certified investment adviser for your investment decisions. Please read disclaimer towards the end of blog.