A good post on sanjay bakshi’s blog on one of the physcological tendencies described by charlie munger.

A good post really worth reading

Good post by sanjay Bakshi

G

A good post on sanjay bakshi’s blog on one of the physcological tendencies described by charlie munger.

A good post really worth reading

Over the years, to get a grip on various elements of investing, I have developed several spreadsheets. Some of these spreadsheets are for screening investment ideas. Some are for carrying out the valuation of a company using various mental models such as DCF (discounted cash flow, Porter’s five factor model etc).

In addition I have some spreadsheets where I try to value the entire market (Sensex or Nifty). I have loaded one such spreadsheet in the new section I have created ‘Quantitative analysis’

In addition to get my arms around various valuation parameters such as ROE, PE, Cash flow, Competitive advantage period and how these parameters work for cyclical, growth and other kinds of companies, I have developed a separate spread sheet which has been added to the same section. This spread sheet titled ‘ROE and PE’ is more of an analysis spread sheet and throws up some obvious and some interesting conclusions.

These spreadsheets and several more which I would be posting are entirely based on my personal understanding of investment concepts and may contain errors. Please feel free to download them, read them and critique them if required. I would be glad if anyone could point out some errors in my thinking as it would help me in refining my understanding of various concepts

I have been reading the book ‘The world is flat’ from Thomas L Friedman. Tom is a New York times columnist who has also written ‘Lexus and the Olive tree’. Both these books are about globalization.

His latest book ‘The world is flat’ is about how the world is changing (he uses the word flattening) due to various trends. I have just completed the first section, which discusses about the various factors, which are driving this trend. The ten key factors, which are driving the world, are below

Tom mentions India a lot in his book. India has definitely got impacted big time. Even individuals like us have benefited. As a personal example – before the net , It was a pain getting financial information on a company. One had to go to a broker, ask for the annual report. The whole research would take days. Now I can Google any company and pull all the data I want.

The transaction costs were high prior to the net. Now the same are below 1 %.

Of course all the information , does not mean that investing is any easier. It still requires interpreting the information. At the same time, the minute-by-minute stock quotes and information (noise ??) are only distracting

It is well documented and known that the pain of loss is much higher than the joy of gain. I have had my share of losses (some due to greed, some due to ignorance). However, as buffet and munger have repeatedly reminded, one should try analyzing one’s mistakes and learn from it.

I am listing some of the errors I have made , and the lessons learnt. My typical holding is 4-5 years and so if I am wrong in analyzing an investment, the impact is much higher for me.

An error of commission

I started investing actively 6 years ago. While reading a magazine, I come across a recommendation for SSI ltd. This was (is ??) a company in the computer education business competing with the likes of Aptech and NIIT. The key differentiator for the company was its short term courses in Java and other technologies which were useful for IT professionals to land a good job. It was selling at a PE of 50 at that time.

The balance sheet was strong , with low debt and the company had recently made an acquisition in the US using its stock (@ a price of 2200 rs / share). The acquisition enabled the company to get into IT services and would have served as a good additional revenue stream.

Shortly after I bought the stock, the Dotcom bubble burst. Recruitments by IT companies slowed down and the IT services market dried up. As a result SSI got hit by a double whammy. Their education business suffered big time and also their IT services company never scaled up in the tough environment. I bailed out of the stock after losing more than 90 %.

My learnings

An error of understanding a catalyst event in unlocking value

My next big mistake did not result in my losing money. But more so, I lost out on a huge gain. The stock is L&T. I bought the stock back in 1998. The company had mediocre performance till then. Post 1998, the performance nosedived. The cement division was doing badly due to the demand supply mismatch and the engineering division was doing average due to a recession in the capital goods market.

On top of that the management, stubbornly kept diverting capital from a high return business (capital goods) to Cement (commodity with low returns). There were media reports that the management would spin off the cement division (but I think it was just a ruse played by the management). Eventually I got disgusted with the management and sold off at minor profit.

A few months later, the Kumarmangalam birla group , after a corporate battle , bought out the cement division. The management (as expected) went ahead and allocated 10% of the equity to the employees and added a poison pill to prevent a repeat takeover attempt (The management is still anti shareholder and I have not changed my mind on that). However with the cement division out of the way, and the capital goods market doing well, the performance improved and the stock has gone up by 8-9 times.

My learning

I will keep listing more of my investing miscues (which I have many) and share my learnings. Please feel free to share yours …

Read this article on cnet.com. The article talks of the challenge which google is posing to Microsoft.

Found the following comment interesting. Interesting to see how established business models are getting disrupted constantly , for ex in Telecom, in the desktop space (where Microsoft had a complete monopoly).

Microsoft, it seems, is faced with a classic “innovator’s dilemma,” as author Clayton Christensen put it in his groundbreaking book that defined why tech giants usually miss the next wave of innovation. Microsoft execs made what looked like the right decisions at the time. As a result, the cash came in. The core product, Windows, became bigger and more complicated, and getting updated versions became harder to get out the door.

Plotting the counter-offensiveThe burden of that success, as the theory in the book goes, makes it harder to respond to the next generation of tech innovators. Years ago, Microsoft and Apple rattled IBM. Now Google, some believe, has a chance to rattle Microsoft by providing a cheaper, easier-to-use alternative. “Every other time Microsoft was attacking from below,” said one former executive. “Now (Microsoft) is being attacked from below and they don’t know how to deal with it.”

Can’t think of an equivalent scenario in India. But models which are undergoing a lot of change are retail, the auto industry – auto parts, Pharma industry (we seem to be playing a role in impacting the global industry ). Good to realize that in most of these sectors, Indian companies are acting as the disrupters or would be disrupters.

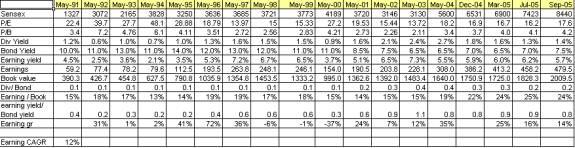

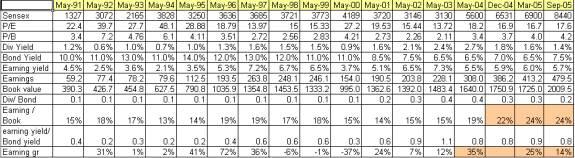

I have been asking this question time and again to myself . Am I being too pessimistic ? I have some statistic below which I calculate to see how the over all market is looking like in terms of valuation and fundamentals ( extending back to 1991) Return on capital, earnings growth seems to be at an all time high. The earnings have more or less doubled in the last 2 years. As a result the valuation do not seem to be stretched. The market is definitely not as richly valued as 2000 or 1992-93. At the same time the earnings growth , return on capital and interest rates are much lower than what we had at that point of time.

Return on capital, earnings growth seems to be at an all time high. The earnings have more or less doubled in the last 2 years. As a result the valuation do not seem to be stretched. The market is definitely not as richly valued as 2000 or 1992-93. At the same time the earnings growth , return on capital and interest rates are much lower than what we had at that point of time.

At the same time, will it get any better going forward. Can the Return on capital improve further, interest rates fall further and earnings growth improve further ? My thought is that the odds are low ….

But does it mean that one needs to sell or the market is ready for a crash ?? again I don’t think that is likely. I have not been able to come to a definitive conclusion and hence have chosen to do nothing ( not buying and not selling ).

Maybe another 10% increase in the market in the next couple of months could change my mind

A great article from Robert J Shiller on china. Just replace china with ‘stock’ of any company and the conclusion reached by Robert makes a lot of sense. The following statement in the article made a lot sense , especially in current context in the Indian market

At times like these, people can easily imagine that an apartment in Shanghai will be worth some enormous amount in 10 or 20 years, when China is vastly more prosperous than it is today. And if it will be worth an enormous amount in 10 or 20 years, then it should be worth a lot today, too, since real interest rates – used to discount future values to today’s values – are still low in China. People are excited, and they are lining up to buy.

To be sure, their reasoning is basically correct. But when the ultimate determinants of values today become so dependent on a distant future that we cannot see clearly, we may not be able to think clearly, either.Since the true value of long-term assets is so hard to estimate, it is human nature to focus on the rate of increase in their observed prices, and to allow one’s attention to become fixated on these assets just as their value is increasing very fast. This can lead people to make serious mistakes, paying more for long-term assets than they should, even assuming that the economy will perform spectacularly well in the future

Is China’s Economy Overheating?

Robert J. Shiller

The Chinese economy has been growing at such a breathtaking annual pace – 9.5% in the year ending in the second quarter of 2005 – that it is the toast of the world, an apparent inspiration for developing countries everywhere. But is China getting too much of a good thing?

Since he became president in 2003, Hu Jintao has repeatedly warned that China’s economy is overheating, and his government has recently acted accordingly, raising interest rates last October, imposing a new tax on home sales in June, and revaluing the Yuan in July.

But claims that China is overheating don’t seem to be based on observations of inflation. While China’s consumer price index rose 5.3% in the year ending in July 2004, this was due primarily to a spike in food prices; both before and since, inflation has been negligible.

Nor are these claims based on the Chinese stock market, which has generally followed a downward path over the past few years.

Instead, those who argue that the Chinese economy is overheating cite the high rate of investment in plant and equipment and real estate, which reached 43% of GDP in 2004. On this view, China has been investing too much, building too many factories, importing too many machines, and constructing too many new homes.

But can an emerging economy invest too much? Doesn’t investment mean improving people’s lives? The more factories and machines a country has, and the more it replaces older factories and machines with more up-to-date models, the more productive its labor force is. The more houses it builds, the better the private lives of its citizens.

A number of studies show that economic growth is linked to investment in machines and factories. In 1992, Bradford DeLong of the University of California at Berkeley and Lawrence Summers, now President of Harvard University, showed in a famous paper that countries with higher investment, especially in equipment, historically have had higher economic growth. One of their examples showed that Japan’s GDP per worker more than tripled relative to Argentina’s from 1960 to 1985, because Japan, unlike Argentina, invested heavily in new machinery and equipment.

In short, the more equipment and infrastructure a country is installing, the more its people have to work with. Moreover, the more a country invests in equipment, the more it learns about the latest technology – and it learns about it in a very effective, “hands-on” way.

It would thus appear that there is nothing wrong with China continuing to buy new equipment, build new factories, and construct new roads and bridges as fast as its can. The faster, the better, so that the billion or so people there who have not yet reached prosperity by world standards can get there within their lifetimes.

And yet any government has to watch that the investment is being made effectively. In China, the widespread euphoria about the economy is reason for concern. Some universal human weaknesses can result in irrational behavior during an economic boom.

Simply put, China’s problem is that its economic growth has been so spectacular that it risks firing people’s imaginations a bit too intensely. At times like these, people can easily imagine that an apartment in Shanghai will be worth some enormous amount in 10 or 20 years, when China is vastly more prosperous than it is today. And if it will be worth an enormous amount in 10 or 20 years, then it should be worth a lot today, too, since real interest rates – used to discount future values to today’s values – are still low in China. People are excited, and they are lining up to buy.

To be sure, their reasoning is basically correct. But when the ultimate determinants of values today become so dependent on a distant future that we cannot see clearly, we may not be able to think clearly, either.Since the true value of long-term assets is so hard to estimate, it is human nature to focus on the rate of increase in their observed prices, and to allow one’s attention to become fixated on these assets just as their value is increasing very fast. This can lead people to make serious mistakes, paying more for long-term assets than they should, even assuming that the economy will perform spectacularly well in the future. They can overextend their finances, fall victim to promotions, invest carelessly in the wrong assets, and direct production into regions and activities on the basis of momentary excitement rather than calculation of economic fundamentals.

So, maybe the word “overheated” is misleading. It might be more accurate to say that public attention is over-focused on some recent price changes, or over-accepting of some high market values. Whatever one calls it, it is a problem.

Fortunately, people also tend to trust their national leaders. For this reason, it is all the more important that the leaders not remain silent when a climate of speculation develops. Silence can be presumed to be tacit acceptance that rapid increases in long-term asset price are warranted. National leaders must speak out, and they must match their words with concrete actions, to help signal to the public that the speculative bubble cannot be expected to continue.

That is what the Chinese government has begun to do. The real-estate boom appears to be cooling. If the government continues to pursue this policy, the salutary effects in terms of public trust in the country’s businesses and institutions will help ensure stable, sustainable economic growth for years to come.

Robert J. Shiller is Professor of Economics at Yale University, Director at Macro Securities Research LLC, and author of Irrational Exuberance and The New Financial Order: Risk in the 21st Century.

Copyright: Project Syndicate, 2005.www.project-syndicate.org

I have been working on various permutations of ROE and CAP (period for which the company can earn over cost of capital) using the DCF model to see the PE ratios which are thrown up by the model.

Its fairly intuitive that a company with a high CAP and high ROE should have a high PE. But these permutations have thrown a few insights

So any time I see a company with PE of 20 or higher (which is high these days), the first question I ask is – Given the ROE of the company, does the company have substantial duration of CAP ( 10 years or higher ).

A company with a PE of 30 or higher must have a great return on capital, very strong growth and 10 years or higher CAP. A point worth thinking about when looking at such high valuation companies.

This way of think is detailed in the book ‘expectations investing’ by micheal maubossin and is definitely worth a read.

I have finally been able to figured out how to provide file downloads from my blog (via yahoo briefcase).

I have a substantial reading material on buffett, Munger, Graham and other investing greats. I have initiated uploading this material under the various sections on the sidebar. Please look under ‘buffett resources’ today for some additional material. I will be continously loading additional material going forward

So stay tuned and hope you enjoy reading the uploaded material.

Please feel free to share thoughts, comments, views and suggestions on how i can improve it my blog further

Pidilite declared a 1:10 split recently. The stock market reacted favorably and has bid the shares to 93 (930 pre-split). The split is hardly a value creation event. Just divides the cake (or pizza if you like the analogy) into more slices. Really does not enlarge the cake. So the company now sells at a PE of 26. Definitely not undervalued …I would say overvalued or at best fairly valued

Time to look at selling the stock ?? I think so ….

{kind=link}

{kind=link}