Bear markets are a good time to reflect !

In a bull market, any pick – good or bad, goes up and everyone feels like a genius. However at times like now, where any kind of mistake is brutally punished, it is easier to uncover flaws in one’s investing process.

So, I have been thinking about my investing process and have realized that one part of my process is exceedingly weak – The selling process

Why should one worry about the process ? If you are interested in understanding it in more detail – read this noteon ‘process versus outcome’. In a nut shell, if you get the investing process right, the outcome (investment returns) will take care of itself. It is the equivalent of getting your batting technique right, if you want to be a good batsmen and get high scores consistently.

As most of you are aware, I am heavily influenced by warren buffett and his investment philosophy. My introduction to investing was through his ‘shareholder letters’ and as a result, I have taken his teachings to the heart.

One of the key tenets of buffett’s philosophy is buy and hold, where one looks for companies with sustainable competitive advantage and buys them at a reasonable price. Once you make the purchase, buffett advises the investor to hold for long periods of time (provided the business maintains its competitive position)

The above is a very sensible approach and would work for majority of the investors. At the same time, the key point in the ‘Buy and hold’ philosophy is to buy a high quality company where the intrinsic value is growing and let time do its magic (via compounding).

A differentiated approach

It has become slowly dawned on me (I am slow learner J), that one needs a more nuanced approach to sell, depending on the nature of the investment. In the rest of this post and the next, I will try to categorize the various types and look at the sell approach one needs to adopt for each of them – This is ofcourse a work in progress and by no means any kind of rule set for me.

Such companies look cheap when the economy is doing well and expensive when things are bad, such as now. If you were to buy and hold such companies over the course of the entire economic cycle (from bottom to top to bottom), the overall returns would be very average. The key in such type of investments is to be able to buy when the company is at or near the bottom of the cycle (difficult to identify usually) and sell as the business recovers – without waiting for the cycle to top.

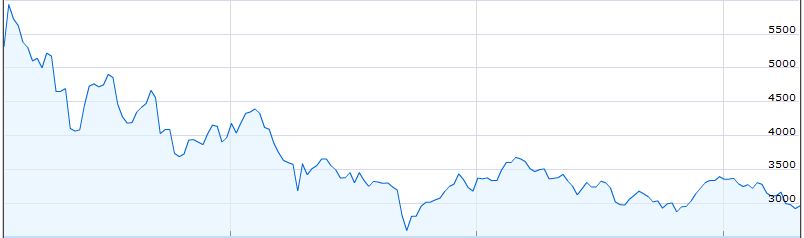

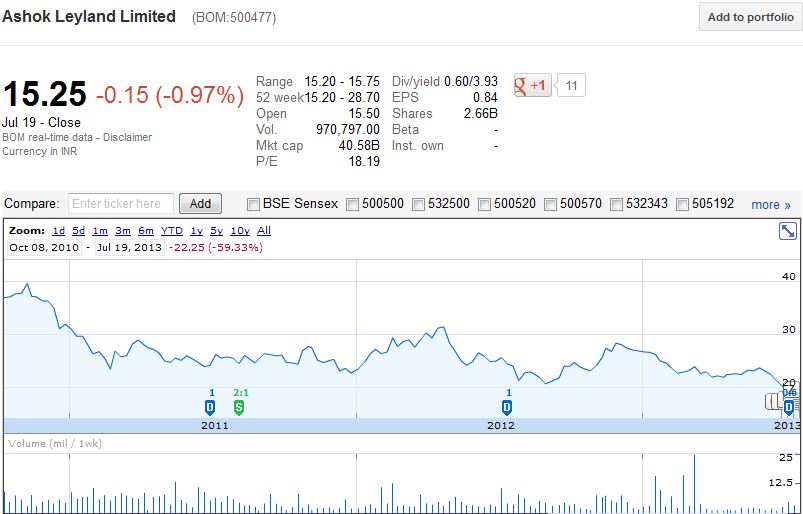

I wrote about the company herein 2008 and kept buying it as the stock crashed during the lehman crisis. My average cost basis was around 11 / share (post split). I was out of the stock by mid 2010. You can see the price action below

The commercial vehicle business turned in 2010 and has been going downhill since then. The stock price has followed suit

So the key point with cyclicals is this – Buy and hold does not work (usually) and timing is critical for above average returns

—————

Stocks discussed in this post are for educational purpose only and not recommendations to buy or sell. Please contact a certified investment adviser for your investment decisions. Please read disclaimer towards the end of blog.