This is a commonly used, but rarely defined word. I am going to argue in this post that the sole purpose of investing is wealth creation.

What is wealth creation ?

Let’s take a numerical example. Let’s say you have 100 Rs. You can invest it in an FD at around 9-10%. At the end of 5 years, you will have around 161 Rs. We can call this the baseline level of return .

However putting money in a Bank FD is not a riskless transaction. If the inflation during this period turns out to be 11%, then you would have lost 5% of your buying power. On the other if we take the average inflation of the last 20 odd years, then the buying power would have risen by 15% over the same period.

Have you created wealth in the above case ? I would say yes, as you have been able to increase your buying power over the investing period, but not by much (15% at best on average).

Let’s say one were to invest in the stock market (via index funds) for a 5 year period. On average, the market has returned around 15-17% per annum over the last 20+ years. If you back out an inflation assumption of 7%, then the buying power would rise by 61% for the period. Now we are talking of some serious wealth creation !

However the above example has a catch – I spoke about an average return of 15-17%. The reality is that the stock market returns are lumpy and you can have a period of 2003-08 of 30%+ returns and then a period of 2% returns for the next 6 years (2008-2013). So in this case, one is talking of wealth creation with an added level of risk.

The above examples are quite obvious , but ignored by many. We need to concentrate on post tax, post inflation returns to evaluate the wealth creation potential of an investment option. If you have a higher buying power after taxes and inflation, then you have created wealth.

The aspect of time

I arbitrarily considered a time period of 5 years in my example. What is the correct period? 1 month, 1 year or 20 years?

I would argue that the time period for wealth creation should be driven by your personal goals. Are you saving (and creating wealth) for the purpose of buying a house or retirement? If that is the case, then the period should be upwards of 10 years.

Let’s put the above two point together – One needs to make a level of post tax, post inflation returns over the investment horizon (10 years +) such that you can meet your personal goals. Why else would you put your money at risk?

Now there a lot of people who invest for the thrill of it (for 100% return in days !!) or to boast of their investing prowess to their friends and impress the other sex , mostly women – who from my personal experience, don’t care about such silly things J ).

It is fine to put your money in the stock market to feel macho about yourself – but let’s not call that investing. Bungee jumping off a cliff is also done for thrills, but no one calls its investing !

Following the logic

If you agree that the purpose of investing is wealth creation over a long period of time, it is important not only to earn high returns, but to also do it consistently over a period of time. There is no point earning 30%+ returns for four years and then losing 50% in the 5th(Which will translate into an 8% annual return)

Why is consistency important ? If you can earn 15% consistently for 20 years, you will have 16 times your starting capital and 40 times if the rate rises to 20% per annum. This is simply the magic of compounding.

Now If you shift your focus from high returns (to feel good or boast about it) to consistent returns (to create maximum wealth), the investing approach changes.

Implication of consistent returns

If you are looking for above average, but consistent returns for the long run what should one look for ? If you are looking at earning a 15-20% return over a 10-20 year period , I would suggest looking for companies which are earning this kind of return on capital now and have the capability to do so for a long period of time.

If you can find a company which has a sustainable competitive advantage (sustainable being the key) or a deep and wide moat, then it is likely to maintain its current high return on capital. If you buy such a company at a reasonable price (around the median PE value for the company), the results are likely to be good over time.

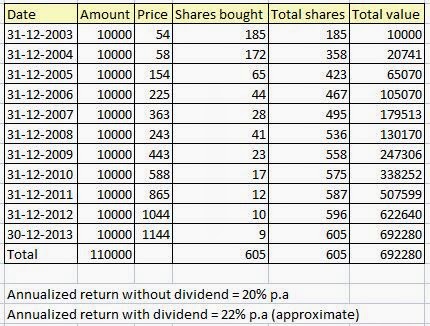

Let’s look at an example here – This is a current holding for me and not a stock tip. The name is Crisil.

You can read the analysis here.Following is a table of price, and annual return/ CAGR for the last 10 years

As you can see, even if you purchased the company on 31stDecember each year (blindly without worry about valuation), you would have done well. This result boils down to the following reason

– The company has a wide and deep moat in the ratings industry due to government mandated entry barriers (none can just start a ratings agency), Buyer power (Companies have to pay to get their debt rated and the cost is usually a small percentage of the debt) and lack of substitutes (even banks insist on company ratings now based on RBI directive).

– The deep and wide moat has enabled the company to maintain a high return on capital of 50%+ for the last 10 years. The company has been able to re-invest a small portion of its profits to fund its growth and has returned the excess capital to shareholders via dividends and buybacks.

A strong competitive position and good management with rational capital allocation approach has resulted in a very good result for the shareholders.

The catch

There always a catch in investing – nothing is as easy as it looks. For starters, this approach requires a huge dose of patience.

How many active investors (me included) would like to select a stock once in a few years and then do absolutely nothing for a long period of time ? In every other profession, progress is measured by level of activity – except investing, where sometimes doing nothing is much better.

The other catch is that this approach is very boring. You find a few companies like crisil and then spend maybe 1 hr each quarter and a few hours every year end reviewing the progress. If the company is still performing as it always has, you have no further work left. If you are a professional investor, what are you going to do with the rest of your time ??

The last catch is that this approach has a level of survivorship bias. If you select a wrong company or if the competitive advantage is lost during the holding period, then the returns are likely to be poor or even negative.

Returns over entertainment

Although this ‘rip van winkle’ approach makes a lot of sense, I am unlikely to follow it fully. I enjoy the process of investing, looking for new ideas and doing all kinds of experiments. At the same time, a major portion of my portfolio is slowly moving towards such long term ‘wealth creation’ ideas.

In the final analysis, investing should be about wealth creation and achieving your financial goals.

—————-

Stocks discussed in this post are for educational purpose only and not recommendations to buy or sell. Please contact a certified investment adviser for your investment decisions. Please read disclaimer towards the end of blog.