Some excerpts from my annual review to subscribers. Hope you will find it useful

Sources of outperformance

Superior performance versus the indices can usually be broken down into three buckets

a. Informational edge – An investor can outperform the market by having access to superior information such ground level data, ongoing inputs from management etc.

b. Analytical edge – This edge comes from having the same information, but analyzing it in a superior fashion via multiple mental models

c. Behavioral edge – This edge comes from being rational and long term oriented.

I personally think our edge can come mainly from the behavioral and analytical factors. The Indian markets had some level of informational edge, but this edge is slowly reducing with wider availability of information and increasing levels of transparency.

We aim to have an analytical edge by digging deeper and thinking more thoroughly about each idea. However in the end, it also depends on my own IQ levels and mental wiring, which is unlikely to change despite my efforts.

The final edge – behavioral is the most sustainable and at the same the toughest one to maintain. This involves being rational about our decisions and maintaining a long term orientation. If you look at the annual turnover of mutual funds and other investors, most of them are short term oriented with a time horizon of less than one year. In such a world of short term incentives, an ability to be patient and have a long term view can be a source of advantage.

How does patience help?

Take a look at the 5 years history one of our oldest positions – Cera sanitaryware.

The company has performed quite well in terms of profits in the last 5 years and grew its net profit by 30% in FY 15 and 23% in FY16. Compare this with the stock price – The stock dropped from a peak of around 2500 in early 2015 to a low of 1500 in the span of one year, even though sales and profit continued to grow at a healthy pace.

These swings are usually due to short term momentum traders who want to move from company to company to catch the incremental 10%. I am glad that we have such investors in the stock market as it gives us an opportunity to buy from time to time when the price drops below our estimate of fair value.

We will continue to get such kind of opportunities in the future. The key is to be patient and act when an opportunity is presented.

Skin in the game

It is not easy to remain focused on the long term. In my case, I do not feel any pressure to negate this advantage and let me share why.

The reason for holding onto this approach is that this is something which has worked for me over 20 years and for others over a much longer period. If one can identify good quality companies at a reasonable price, then the returns over the long term will track the performance of the business (more on it later in the note). The value approach works over time, even if it does not work all the time

In addition to the above, my own net worth and that of my close friends and family is invested in the same fashion. I will not take the risk of blowing up to show short term results. Nothing focuses your mind, when your own net worth and that of friends and family is invested in the same fashion.

Let’s try to understand the math behind my expectations of the long term returns. This is a repeat for some of you, but is worth reading again.

The math behind the returns

At the time of starting the model portfolio, I stated 3-5% outperformance as a goal and this translated to around 18-21% returns over time. How did I come up with this number and more importantly does it still hold true?

Let’s look at the math and the logic behind it. The outperformance goal ties very closely with my portfolio approach and construction. We typically have around 15-18 stocks in the portfolio, bought at 60-70% discount to intrinsic value on average. Most of the companies we hold have an ROE of around 20-25% and are growing around 18-20% annually. These numbers may vary, but on average they will cluster around the above figures over time.

Let’s explore a specific example based on these numbers. Let’s say a company valued at 100, growing at around 20% is purchased for 70. Let’s assume I am right in my analysis and the stock converges to fair value in year 3. If this happy situation comes to pass, the stock will deliver around 34% per annum return.

Now in year 3, we could sell the stock and buy a new one again and make similar returns. This may occur from time to time in individual cases, but is not feasible at the portfolio level unless the market is in the dumps and stocks are selling at cheap prices. It is unlikely that our positions would be in a bull market and selling at full price, when other stocks are available at a discount.

In such a case, if the quality of the company is high and we continue to hold on to it, it will deliver a return of around 20% per annum in the future (assuming the stock continues to sell at fair value going forward). If you add 2 % dividend to this 20% annual increase in fair value, the stock could deliver around 22% for the foreseeable future.

The portfolio view

The math, explained for a single stock, works at the portfolio level quite well. As per my rough estimates, the model portfolio has grown at around 22% per annum in intrinsic value. It was selling at around 27% of intrinsic value when we started and is at a 20% discount now. You have to keep in mind that there are just estimates on my part and I cannot provide any mathematical proof for it. However I have found that these two variables have worked quite well in understanding the performance of the portfolio over the long run – discount to intrinsic value and growth of the value itself.

As the intrinsic value has grown over years and the gap closed, we have enjoyed a tailwind and hence the returns have been a bit higher than that of the intrinsic value. The returns are often lumpy as can be seen from the performance.

Where will these returns take us?

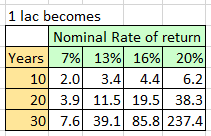

If you talk to some investors, they would scoff at 20% returns. Let look at this table for a moment

I am sure a lot of you have seen the above table. It shows how much 1 lac will become if you allow it to compound at a certain rate of return for 10, 20 and 30 years.

There is something different in the table, from what you would have normally seen. The rate of return numbers seem to be random – 7%, 13% etc., but they are not. Let’s look at what they signify

7 % – This is normally the rate of return one would get from a fixed deposit in the bank

13% – This is the average rate of return from real estate over long periods of time. I would get eye rolls when I quoted this number in the past. The recent and ongoing experience is changing that now.

16% – this is roughly the kind of return you can get from the stock market index over long periods of time

20% – This the level of returns we ‘hope’ to achieve in the long run (3+ years or more)

There are a few key implications of the above table

– A small edge over average returns adds up to a lot over time

– The key to creating wealth in the long run is not just super high returns, but to sustain above average returns over a long period of time. It is of no help if you compound at 30% for 20 years and then lose 80% of your capital in the 21styear. The key is to manage the risk too.

If we achieve our stated goal over the long term, the end result will be quite good. There are two risks to this happy end – avoid blowing up (which I am focused on) and early retirement (mine), which you have to hope does not happen either involuntarily (I get hit by a bus) or voluntarily (I head off to the beach).

—————-

Stocks discussed in this post are for educational purpose only and not recommendations to buy or sell. Please contact a certified investment adviser for your investment decisions. Please read disclaimer towards the end of blog